9月12日,《華爾街日報》、《財星》雜誌、《彭博商業週刊》三大國際財經媒體,斗大的新聞標題上,居然同時出現韋斯勒(Ted Weschler)這個大眾全然陌生的名字。這一天前,韋斯勒只是個擁有高額財富的基金經理人。但現在,韋斯勒擁有了眾人欽羨的新身分。

巴菲特的波克夏公司,在9月12日正式發出新聞稿,指定他為巴菲特的接班人選。為何,股神選上韋斯勒?

多年協助巴菲特撰寫波克夏公司股東信,也是《財星》雜誌資深主筆的盧米斯指出,假設投資人在2000年,也就是韋斯勒創立半島資本顧問公司的第一年,就投資此基金,到今年第一季,11年來獲得的總報酬率竟高達1236%。

這樣突出的績效,當然讓股神另眼相看。

但,韋斯勒不僅是投資績效優異,事實上,他在投資策略和個人風格上,也和巴菲特有許多相似之處。

根據各基金公司每季向美國證監會的申報資料,韋斯勒基金目前約19億6000萬美元的持股總額中,只投資包括北美第一大衛星電視業者直接電視公司、1953年於紐約交易所上市的老牌化學原料公司格雷斯等九檔股票。平均在一檔股票上,就投資超過兩億美元,也就是新台幣60億元。

不僅如此,這九檔持股中,居然有兩檔已經連續持有超過八年,其他也持有平均三到五年的時間。在過去十年變動快速、當紅產業不斷更替的投資市場中,這樣「以靜制動」的做法,看似不合常理,但卻與巴菲特曾描述自己「近乎怠惰的按兵不動」投資風格,完美配對。

若說,長期抱股,是股神與接班人的第一個共通處。不眷戀繁華的紐約大都市,選擇在小城裡開始自己的投資事業,則是兩人第二個相同點。

巴菲特在紐約哥倫比亞商學院取得碩士學位後,一開始在投資名人葛拉漢位於紐約的投資公司工作。兩年後,年逾60的葛拉漢決定退休,而26歲的巴菲特,也決定回到美國中部的家鄉奧馬哈,開始自己的投資事業。

而韋斯勒在28歲時,也就是1989年,首次創立自己的基金投資公司。當時網際網路也不如現今發達,但韋斯勒卻選擇在距離紐約500公里,維吉尼亞州一個人口不到五萬人的小城,夏洛特斯維爾,開始他的投資生涯。

此外,巴菲特對報業經營,也有著特殊感情。他在19歲念大學時,就在家鄉的《林肯日報》擔任小主管,管理送報生,1969年更買下家鄉報紙《奧馬哈太陽報》。在巴菲特的傳記書中,就曾提及,假如巴菲特不從事投資,那最有可能從事的就是新聞工作。

而早在十年前,韋斯勒除基金操盤外,就與友人共同創辦夏洛特斯維爾的一份當地報紙,做為私人投資。除了參加每季會議,也在報社的財務議題上,給予建議。

在今年7月26日,兩人第二次「巴菲特午餐」約會時,巴菲特主動對韋斯勒提出到波克夏任職的邀請。股神對媒體表示,其實自己對於韋斯勒是否接受提議「並沒有多大把握」,因「他已在自己的基金中,賺到很多錢了,你可以從他的投標金額中看出。」

但以韋斯勒在短短一週內,就接受這份邀請看來,股神的魅力,凡人的確無法擋。

股神接班人添猛將!Ted Weschler出線 10年投報率1236%

股神接班人又添一名,避險基金經理人 Ted Weschler 出線,擅長多空交易策略,其投資報酬率自 2000 年至今高達1236%。據《彭博社》12日報導,巴菲特雇用避險基金經理人 Ted Weschler 協助管理海外投資,接班人選再添一位。

現年 50 歲的 Weschler 向自己的避險基金合夥人表示,將關閉自己的避險基金,並在明年初加入波克夏旗下。

波克夏雇用 Weschler 是為了分攤現年已 81 的巴菲特的負擔。巴菲特作為波克夏的投資長,工作量是三個基金經理人的量,而在去年巴菲特也雇用了一位避險基金經理人 Todd Combs。

在巴菲特卸任之前,波克夏將再添一位基金管理人,日後將與Weschler 與 Todd,共同負責波克夏的投資組合。據 6 月 30 日資料,波克夏投資組合的淨值高達670 億美元。

Ted Weschler 的避險基金報酬率從 2000 年到今年第一季的數字是1236%,操作風格是買進或放空上漲跟下跌的股票。他在投資領域的才幹先被 《Fortune》記者 Carol Loomis發現,進而被巴菲特相中。

Loomis 是巴菲特的多年摯友,同時也是每年波克夏股東信的撰稿人。他兩度發現 Weschler 參加與巴菲特晚餐的競標。這兩次競標共花了Weschler 超過 500 萬美金。

據了解,巴菲特的下一位接班人選,可能會挑選在債券領域有專長的經理人,因波克夏投資組合中包含了超過 350 億美元的債券標的。(鉅亨網)

How would you feel about taking a pay cut and paying more in taxes?

Meet Ted Weschler. He just did both. And he’s happy about it.

You might have heard about Mr. Weschler. He was hired by Warren E. Buffett last week to help invest Berkshire Hathaway’s piles of cash.

Mr. Weschler, a successful but little-known 50-year-old hedge fund manager, plied his trade from a small office in Charlottesville, Va., above an independent bookstore, reaping huge returns for his investors, some 1,236 percent over a decade. In the process, his $2 billion fund put him comfortably in the millionaires’ club, and at the rate he was going, he was on his way to the more exclusive cadre of billionaires.

Here is a quick measure of his wealth: he paid $2,626,311 in a charity auction to have lunch with Mr. Buffett in 2010. That’s how they met. A year later, Mr. Weschler paid $2,626,411 to dine with him again.

In his new job at Berkshire, he is expected to be paid significantly less than he was making. (We’ll get to the formula for his compensation in a moment.) And he is going to be giving up a huge tax break. Instead of paying the 15 percent capital gains rate on most of his income like most hedge fund managers and private equity executives, he is going to be taxed at the 35 percent ordinary income level as an employee.

His decision — and his compensation structure — are worth considering as the country weighs President Obama’s proposal to increase taxes for the ultra wealthy in what has been called the “Buffett Rule.”

The plan is aimed at ensuring that millionaires pay the same effective rate as middle-income families. In part, it takes aim at the controversial “carried interest” income, or the profits that hedge fund managers and other big investors take home as part of their pay. That compensation is now taxed at the capital gains rate of 15 percent, far below the 35 percent top rate on ordinary income. Mr. Obama hopes to close that loophole.

Many Republicans have derided the Buffett Rule, saying it would hurt the economy. “If you tax job creators more, you get less job creation,” Representative Paul D. Ryan, Republican of Wisconsin, argued on “Fox News Sunday. “If you tax investment more, you get less investment.”

Perhaps Mr. Ryan should dine with Mr. Weschler. The view that “millionaires and billionaires” will stop, or slow down, working or investing may be a myth.

“When you have enough money to live the lifestyle you want,” Mr. Weschler told me in a brief conversation, money and taxes are less of a consideration than “who you want to work with.”

Mr. Weschler — and his colleague Todd Combs, another successful hedge fund manager who joined Mr. Buffett last year — demonstrate that people of great wealth don’t necessarily make all decisions based on their own financial bottom line.

“Neither would have voluntarily paid more than 15 percent when working at their hedge fund simply because of the feeling that they were a favored class,” Mr. Buffett said. “But neither will feel the least bit abused because the earnings from their daily labors will now be taxed at a higher rate.”

Like Mr. Buffett, Mr. Weschler says he doesn’t believe the tax loopholes for hedge fund managers make sense. “When my accountant first told me about it,” he said he responded “You can’t be serious.” But he added quickly, “I’m not complaining.”

That’s not to say he will be paid like a pauper at Berkshire. Mr. Weschler and Mr. Combs will earn seven figures, and potentially more. But they won’t make John Paulson money. He reportedly made $5 billion last year.

Unlike hedge fund managers, at Berkshire Mr. Weschler and Mr. Combs don’t take home the standard “2 and 20,” collecting a 2 percent management fee and 20 percent of all the profits. Instead, Mr. Buffett has tightly linked their pay to the performance of the Standard & Poor’s 500-stock index, a system that some big institutional investors should be pressing hedge funds to adopt.

“Both Todd and Ted will have performance pay based on 10 percent of the excess return over the S.&P., averaged over multiple years,” Mr. Buffett told me. “If the S.&P. averages 5 percent annually in the future, this means that the average hedge fund manager has received a 1 percent performance fee — 20 percent of 5 percent — before Todd and Ted receive anything.”

“Nevertheless, I expect them to make a lot of money,” he added. “The difference is that they have to earn it by true investment performance.”

In addition, both men receive modest salaries that Mr. Buffett said “will work out to about a tenth of 1 percent” of the assets they manage. “This compares to the 2 percent nonperformance fee which most hedge fund managers charge, even if they are losing money.”

Mr. Buffett’s critics complain that while he supports higher taxes on the wealthy, Berkshire is structured to pay little in taxes and he has sidestepped Uncle Sam by giving away his wealth.

Some have even suggested that he mail the Treasury a check if he wants higher taxes. The Senate minority leader, Mitch McConnell, Republican of Kentucky half-jokingly said on NBC News program “Meet the Press,” “if Warren Buffett would like to give up some of his benefits, we’d be happy to talk about it.”

But Mr. Buffett shrugs off the naysayers. “When I ran my partnership in the 1950s-1960s, I was generally taxed at 25 percent, considerably below the rate on similar amounts of ordinary income,” he said. “I knew I was getting favored treatment compared to the local doctor, lawyer or C.E.O., but I made no voluntary payments to the Treasury, nor does any hedge fund manager of whom I’m aware.”

A Look At Buffett Pick Ted Weschler's Portfolio Holdings

Warren Buffett has tapped Ted Weschler to manage a piece of Berkshire Hathaway's (BRK.A)(BRK.B) investment portfolio. Weschler has been managing partner of Charlottesville, VA-based value-oriented hedge fund Peninsula Capital Advisors.

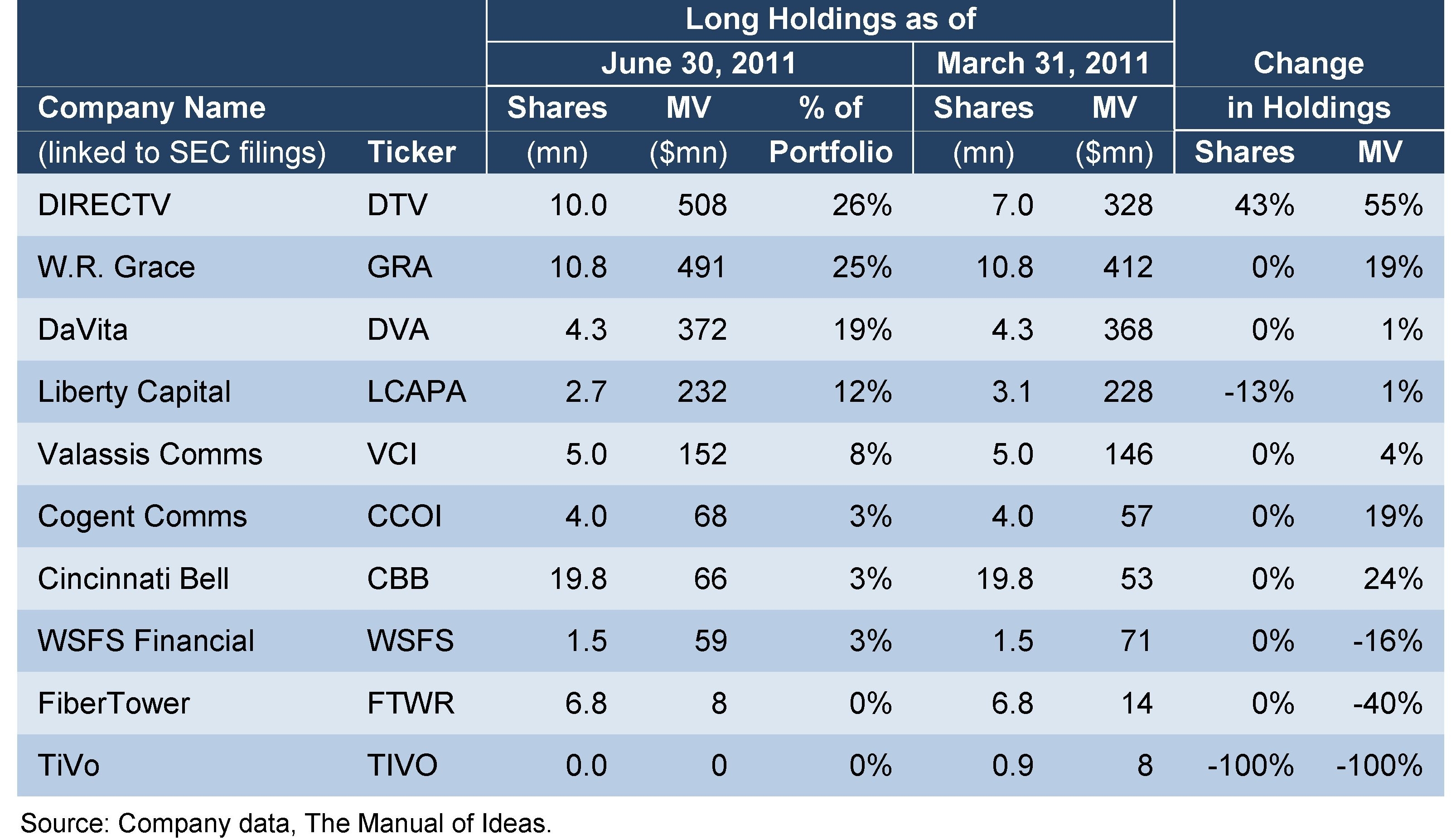

Here is a look at Weschler's long equity holdings at the end of Q2. Of note is the high concentration of the $2 billion stock portfolio, with one-half of the disclosed portfolio invested in just two companies -- DirecTV (DTV) and W.R. Grace (GRA). Both companies' stock prices advanced during the second quarter.

Peninsula Capital Advisors – Long Portfolio, June 30, 2011

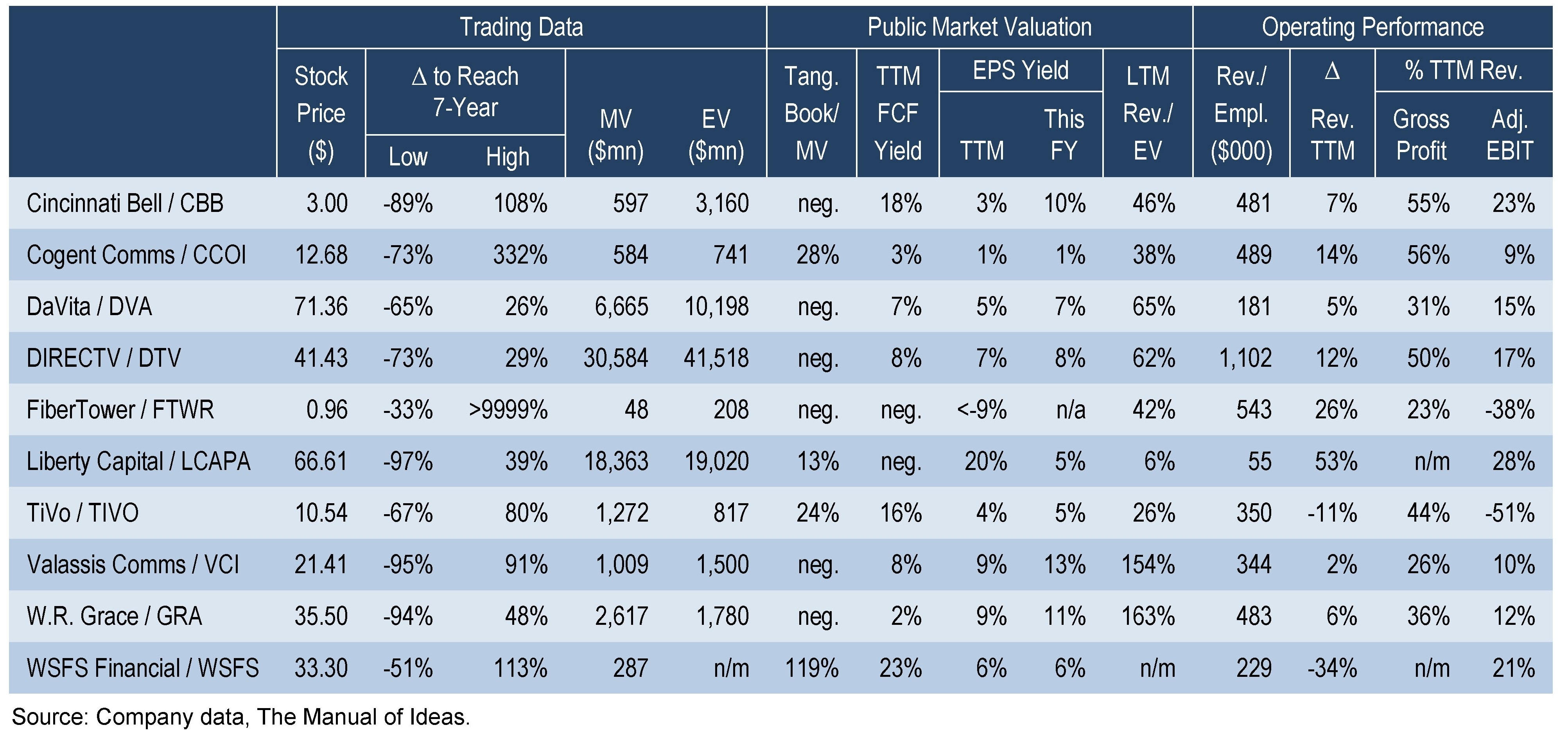

We also present a snapshot of key trading, valuation and performance metrics of the companies in Peninsula's long portfolio. Of note is that most of the companies have negative tangible book value, a sign that Weschler may be more of a Buffett-style "quality-at-a-reasonable-price" investor than a Graham-style deep value investor.

Peninsula Capital Advisors – Selected Data on Portfolio Companies

Finally, we note that it is highly unusual for a die-hard value investor and Buffett follower such as Weschler to remain nearly anonymous within the value investment community, especially considering Peninsula's fairly large assets under management ($2+ billion). The fact that Weschler insisted on being an anonymous bidder for the charity lunch with Buffett in 2010 and 2011 only underscores the degree to which Weschler has preferred anonymity within the fairly tight-knit value community. This non-promotional attitude must have appealed to Buffett.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

留言列表

留言列表

{kind=link}

{kind=link}